When we look back over the past three years, investors have earned remarkably similar returns in local currency terms in very different parts of the world.

UK, eurozone, Japanese and emerging market equities have all returned close to 9.5% a year1. The US, as is well known, has been the outlier and star performer, delivering closer to 11.5% a year.

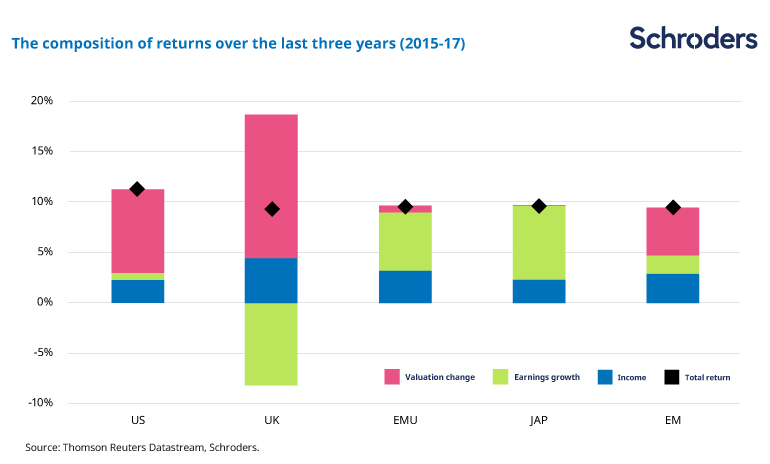

However, when we look behind the numbers at what has been driving that performance, we find an altogether different and more diverse set of circumstances. The chart below decomposes returns over the 2015-2017 period into their key components:

- Income (blue bar) – dividends2

- Earnings (green bar) – how fast have companies grown their earnings?

- Valuations (red bar) – how has price/earnings multiple changed? Does the market now value companies more or less, for a given level of earnings

The sum of these components approximates the return on the stockmarket, which is shown with a black diamond.

Past performance is not a guide to future performance and may not be repeated.

Three key features stand out:

- US returns have been driven predominantly by increasing valuations. Earnings growth has been next to nothing.

- Japanese and eurozone equities have been powered by a combination of strong earnings growth and dividends. The market has failed to reflect these better fundamentals in valuations, which have stagnated.

- UK equities have had a rollercoaster ride. The decline in commodity prices contributed to a collapse in earnings over the past three years, given the market has a large allocation to this sector. However, investors have been prepared to value companies higher relative to those depressed earnings, which has softened the blow. One explanation for this is that investors have priced in a sustained recovery in commodity prices.

When we look at 2017 in isolation we find a different set of drivers. Synchronised and strong earnings growth everywhere has been the main engine of returns in all markets.

So, as investors, what should we make of this? Firstly, the fact that US returns have been so poorly underpinned by fundamentals is a concern. Stellar returns have been built on shaky foundations. This can only go so far but reassuringly, 2017 saw strong earnings growth in the US and 2018 is also shaping up for more of the same. The necessary rebalancing in the drivers of returns is underway, which suggests the rally may yet have legs.

Unloved markets

Elsewhere, it pays to have an eye on those markets that have been somewhat unloved. Despite generating the strongest earnings growth of all markets shown, the valuations of Japanese equities have languished relative to the rest of the world. They are lower at the end of 2017 than a decade earlier. After decades of poor growth, investors have remained somewhat untrusting of the recovery. Should this hold out, then there is more potential here than just about anywhere else for increasing valuations to boost returns.

European equities have also not been hugely rewarded for the earnings recovery that has commenced. Valuations have hardly changed since 2013. Given their earlier stage of the economic cycle, earnings growth is likely to drive returns in 2018 with potential support from valuations.

The UK equity market has been the worst place to be invested from an earnings standpoint. Earnings rebounded sharply in 2017 but remain over 40% lower than their 2007 peak and even 30% lower than after their mini recovery which fizzled out in 2011.

A chunky dividend yield of close to 4% provides a solid base for returns but unless earnings recover, this is unlikely to be sustainable. UK companies paid out 80% of their earnings in 2017 to cover dividends, way above the long-term average of around 50%. Commodity prices have rebounded and both dividends and earnings have a lot riding on that holding out.

The drivers of emerging market equity returns have been reasonably well balanced over the past three years. Valuations have risen but are not as extended as in some other markets and earnings stand to benefit from the synchronised global recovery and weakness in the US dollar. The potential for positive contributions from all factors remains on the cards in 2018.

Earnings growth – a positive driver

At a very high level, the supportive economic backdrop suggests that earnings growth should positively contribute to all markets in 2018.

Dividends are also well supported in all markets other than the UK, which is beholden to commodity prices.

The big differences could arise from valuations. No market is immune to falling valuations but that does not mean returns have to be negative, if the other two drivers contribute enough. A year of solid, if not spectacular, returns could be on the cards.

-

Duncan Lamont is Head of Research and Analytics at Schroders

Important information:

The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 31 Gresham Street, London, EC2V 7QA. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.