Asia has typically been viewed as an investment destination for those seeking capital growth with relatively high levels of volatility. However, against a global backdrop of growing demand for income-related investments, the dividend story developing in Asia remains underappreciated. Could Asia be the future investment destination for your income needs, asks Jochen Breuer, Portfolio Manager, Fidelity Asian Dividend Fund.

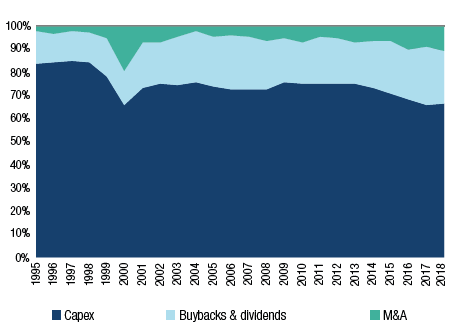

Over the last few years we have seen significant developments from Asian companies in terms of dividend policies, driven by a combination of investor demand, regulatory change and more disciplined capital allocation. While growth is still a key goal for Asian companies and the structural growth opportunities remain, companies are increasingly rewarding shareholders via increasing dividends and buybacks while being more disciplined when it comes to capex decisions.

MAJOR USES OF OPERATING CASH FLOW FROM ASIAN COMPANIES

Source: Jeffries, Factset, August 2019. Aggregates are bottom-up calculated without free float adjustments based on current universe (MSCI Asia e x Japan ex Financials).

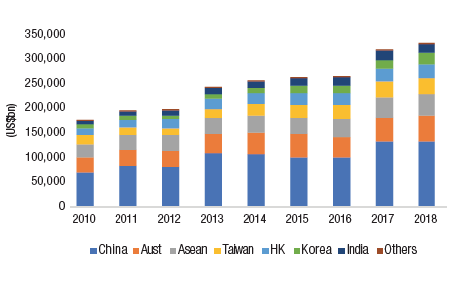

This is generally supported by a more progressive regulatory environment. For example, in China we have seen improving dividend payouts in the last couple of years, especially among state-owned enterprises where it is being driven by government directives. In fact, in US dollar terms Chinese companies are now the second largest payer of dividends globally, forking out over US$145bn to investors via cash dividends in 2018 - UK companies paid out US$115bn over the same period.

Another example is in Korea, where companies face tax penalties for sitting on too much idle cash and tax incentives for putting this cash to work for shareholders. The result has been a rise in dividends and buybacks from Korean corporates.

At the same time, the region has dividend stalwarts such as Australia, driven by demand from local superannuation funds and a very attractive franking credits scheme, as well as Taiwan, where companies face tax disadvantages for retaining earnings.

ASIAN DIVIDEND PAYMENTS HAVE ALMOST DOUBLED IN THE LAST DECADE

Source: Jeffries, Factset, August 2019. Bottom-up aggregated free float adjustments based on current universe (MSCI Asia-Pacific ex Japan). Based on dividends from cash flow statement.

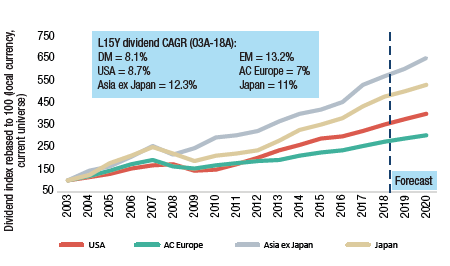

Yields across the region vary, from low yields in India (where the growth opportunity is high and valuations relatively expensive) to global-leading yields in Australia. However, the general trend is higher payouts and - as the chart above shows - the absolute amount of dividends paid out by companies is increasing at a healthy rate. As a result, we have seen superior dividend growth in Asia versus other markets in recent years.

DIVIDEND GROWTH BY REGION - ASIA LEADS THE WORLD

Source: Jefferies, Factset, August 2019. Note: Dividend growth of MSCI regions since 2003 (based on current universe).

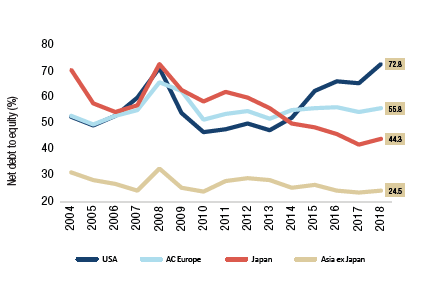

Crucially, dividends are supported by strong balance sheets, which can be traced back to the 1997 Asian financial crisis. During this period companies learned a hard lesson in what happens if you do not allocate capital correctly and borrow for domestic ventures in foreign currency. As a result, Asian companies now enjoy some of the most solid and stable balance sheets in the world, creating a strong foundation for increasing dividend payments.

ASIAN COMPANIES HAVE STRONGER BALANCE SHEETS

Source: Jefferies, Factset, August 2019. Net gearing trend of MSCI regions ex Financials (based on current universe).

Yet it is not just attractive yields supported by solid balance sheets that investors can benefit from. The Asia region is still in its development phase and continues posting economic growth rates above that of developed markets like Europe and the US. Asian companies are able to tap in to this structural opportunity driven by rising incomes, a growing middle-class and demographics to grow further, and as they do they generate more cash for dividend growth.

THE CURRENT ENVIRONMENT - BOND PROXIES TRADING AT HIGH VALUATIONS

We have observed an interesting development across Asia over recent months in that companies which underperformed strong markets in the first part of the year have continued to underperform during a period where sentiment has been impacted by trade tensions and concerns over the health of the global economy.

As a result, we have not witnessed a mean reversion or the swapping of market leaders, despite some significant policy and macro changes. A lot of the names which have underperformed are cyclicals where investors are in no rush to buy, despite cheap valuations, given the increasingly uncertain outlook and subsequent earnings downgrades. Energy names and banks are prime examples of this phenomena.

All the while, we have seen outperformance of so-called “bond proxies” and high-quality compounders (i.e. names with very high earnings visibility). A number of these types of companies now trade on very high relative valuations and as a result it is increasingly difficult to find new ideas in this space.

So where are the opportunities for investors? Looking at markets today, I think valuations in companies who pay lower dividends but with decent dividend or earnings growth prospects look attractive. I also see an interesting middle ground of companies that have traditionally been labelled as defensive, but have continued to underperform, mainly due to stock or country specific reasons. Chinese telecoms and Hong-Kong conglomerates and property stocks fall into this category. This area now offers selective opportunities as relatively low valuations should also provide a decent margin of safety if macro headwinds continue to intensify.

Past performance is not a reliable indicator to future returns.

Jochen Breuer, Portfolio Manager, Fidelity Asian Dividend Fund

Article taken from Hub News Issue 43.

*Based on 12-month gross trailing dividend yield excludes impact of special dividends. Data based on Fidelity Asian Dividend Fund as at 31 July 2019.

Important notice

This information is for investment professionals only and should not be relied upon by private investors. The value of investments and any income from them can go down as well as up so the client may get back less than they invest. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. The annual management charge for the Fidelity Asian Dividend Fund is taken from the fund’s value, so it may give a higher income, but the fund’s capital may decrease, which will affect future performance. The fund can also use financial derivatives which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in small and emerging markets can also be more volatile than other more developed markets. Reference in this article to specific securities should not be interpreted as a recommendation to buy or sell these securities but is included for the purposes of illustration only. Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document and current and semi-annual reports, free of charge on request, by calling 0800 368 1732. Issued by Financial Administration Services Limited and FIL Pensions Management, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM0919/24375/SSO/NA