By Peter Elston, Chief Investment Officer, Seneca Investment Managers

Since the Great Financial Crisis, a period during which the developed world has struggled to grow, there has been much talk about ‘secular stagnation’. Is it a reality?

- There are two major causes of lower growth among developed economies in recent years: the internet and emerging markets.

- Politics will likely accelerate these trends of higher growth and higher inflation. Those left jobless or in low productive work are fighting back by voting for non-mainstream politicians who promise change.

- Higher growth in combination with this shift from labour to capital will mean structurally higher inflation in the developed world for the next few decades.

‘Secular stagnation’ is a reference to economies that are suffering from a chronic shortage of demand and thus cannot grow. On the other hand, there is the optimistic view. Those in this camp believe that the human race will always find ways to do things in a better and more efficient way, thus driving economic growth. Any economic weakness lasting beyond the recession itself would, according to the optimists, be temporary.

I am in the optimists’ corner

There are I think two major causes of lower growth among developed economies in recent years: the internet and emerging markets.

The internet has caused massive and rapid job destruction that has either been obvious – online retailers replacing high street retailers – or less obvious – we as individuals do not rely on intermediaries such as travel agents or bank tellers as we did previously. Those displaced have often taken low productivity jobs, which has meant lower growth. It will take time for societies to work out how to redeploy them in more productive work and to create the necessary education, training and commercial infrastructure. Nevertheless, everywhere one looks one sees innovation – in computing, medicine, energy, transportation, construction. Future generations of university graduates will likely look very different in terms of what sort of jobs they end up in and indeed, what their employers are selling.

As for the second cause, the unleashing of workforces in countries like China and India onto the world stage in recent decades has been hugely deflationary for the developed world. Jobs in the emerging world have replaced jobs in the West, but the emerging world has not repaid the compliment with reciprocal demand for Western goods and services. This effect has shown up in large trade surpluses for many emerging countries, as US president Trump has recently pointed out. He needn’t worry. Emerging countries will at some point reach the stage at which they will want to start spending their bloated foreign exchange reserves which will provide a boost to economies in the developed world.

Politics will likely accelerate these trends. Those left jobless or in low productive work are fighting back by voting for non-mainstream politicians who promise change. Tax avoidance and wealth inequality are also emotive issues that infuriate electorates. The last few decades have seen a gradual shift in income and thus wealth from workers to the owners of capital. We may well be starting to see a shift the other way.

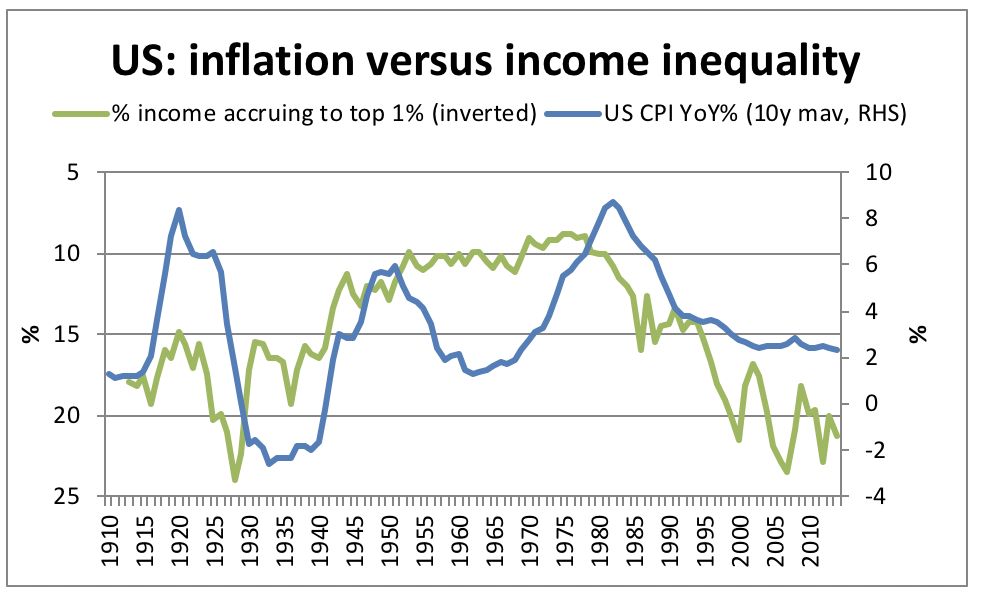

Higher growth in combination with this shift from labour to capital will mean structurally higher inflation in the developed world for the next few decades. Higher growth generally means higher inflation, but falling inequality also tends to be inflationary. In the US, inflation rose from 1930 to 1980 as inequality fell. It then fell throughout the last four decades as inequality rose (see chart). The reason for this relationship is somewhat complex and thus beyond the scope of this article. Better economic growth and falling inequality will be a blessing for many, but the associated higher inflation will likely play havoc with financial asset prices, particularly bonds. From 1940 to 1981, long bonds in the US returned -67% in real terms*. This is equivalent to -2.7% per annum compared with +2.1%* on average over the last 150 years (up to July 2017). If history is to rhyme, as it tends to, multi-asset funds that invest a large portion in bonds are going to face difficulties. It will be important for fund managers to guide their clients’ expectations.

There has been much talk recently around clarity of fund objectives, with the FCA on 5 April providing further guidance on what constitutes good practice. In the wake of the FCA’s report, Jason Broomer, head of investment at Square Mile, said that he found some fund objectives “ludicrous”. "It could be a UK equity fund and the objective they have is to ‘achieve a return by investing in UK equities.’ It is meaningless garbage that has probably been written by a lawyer or someone in compliance and it does not help”, he said.

At Seneca Investment Managers, we take our fund objectives very seriously. For example, the objective of our investment trust, the Seneca Global Income and Growth Trust is:

“Over a typical investment cycle, the Company will seek to achieve a total return of at least CPI plus 6% per annum after costs with low volatility and with the aim of growing aggregate annual dividends at least in line with inflation, through the application of a Multi-Asset Investment Policy”

No one could accuse us of being vague or evasive!

There are no doubt trusts that also have clear and specific objectives, but we think what makes ours unique, and even more credible, is our use of the word ‘typical’.

While it may be a nice idea to target a real return of 6 per cent over an investment cycle, there have been, as I have noted, investment cycles in the past when real returns from equities and bonds have been so poor that achieving 6 per cent real would have been a pipe dream. I think there will be investment cycles in the future in which poor real returns from major asset classes will again render an expectation of decent real returns futile.

In typical cycles when asset class returns are respectable, we are very comfortable telling our investors that 6% real is achievable. Outside this, we think they deserve the truth. High real return objectives that do not take account of the reality of the occasional dismal investment cycle are, we think, disingenuous.

We think it is important to guide our clients’ expectations, but we also believe that by being acutely aware of the challenge for bonds and equities posed by higher inflation, we are in a better position to navigate the trust through the choppy waters that lie ahead. We will do this by often having no or limited exposure to developed country government bonds but also by seeking to add alpha in other ways such as preferring mid cap companies or investing in specialist investment trusts such as REITs or infrastructure trusts that can act as bond proxies (yields can be high and real income streams stable).

Are we right to expect higher inflation in the decades ahead? The term ‘secular stagnation’ was coined by American economist Alvin Hansen in 1938 following two deep recessions in the space of a few years. His view was that the severity of these downturns was evidence of America no longer being able to grow. Had he known the invention of the silicon chip lay just around the corner, he perhaps might have decided not to publish.

Source: http://elsa.berkeley.edu/users/saez/TabFig2012prel.xls, measuring worth.com

*Credit Suisse

Sources:

https://www.ftadviser.com/fca/2018/04/05/fca-lauded-for-attack-on-ludicrous-fund-manager-targets/

https://en.wikipedia.org/wiki/Alvin_Hansen

https://www.measuringworth.com/datasets/uscpi/result.php

https://www.independent.co.uk/news/business/analysis-and-features/